Three of our Best Insights for July

Our Monthly 3-2-1- Newsletter RESOURCE: Preserving Wealth: Chapter One, What are the 7 Key Lessons for Inheritance and Financial Planning? In the first chapter of Preserving Wealth for the Next Generation, we are introduced to a family gathering at their father’s summer cottage in Honey Harbour. It’s the opening weekend of summer, but it’s filled with […]

Three of our best Insights for May

Our Monthly 3-2-1- Newsletter RESOURCE: What are the Retirement Income Investment Options As you transition from your working years to retirement or optional work years, creating a cash flow stream from your investments is critical to retirement planning. There are five main retirement investment options to consider when developing a prudent plan for retirement cash […]

The R6 Retirement Playbook™ A Smarter Way to Retire with Confidence

Retirement today isn’t what it used to be. People are living longer, everything gets more expensive, markets are unpredictable, and tax rules keep changing. That’s why we created the R6 Retirement Playbook™ — a simple, six-part process to help you build income you can count on, reduce taxes, protect your lifestyle, stay flexible, and feel […]

RRSP Maturity Options: What You Need to Know

You don’t have to wait until you’re 71 to convert your RRSP. You can do it anytime before then, depending on what works best for your retirement income strategy. The key is choosing the right option based on your goals, cash flow needs, and tax situation. If you are turning 71 this year, you must […]

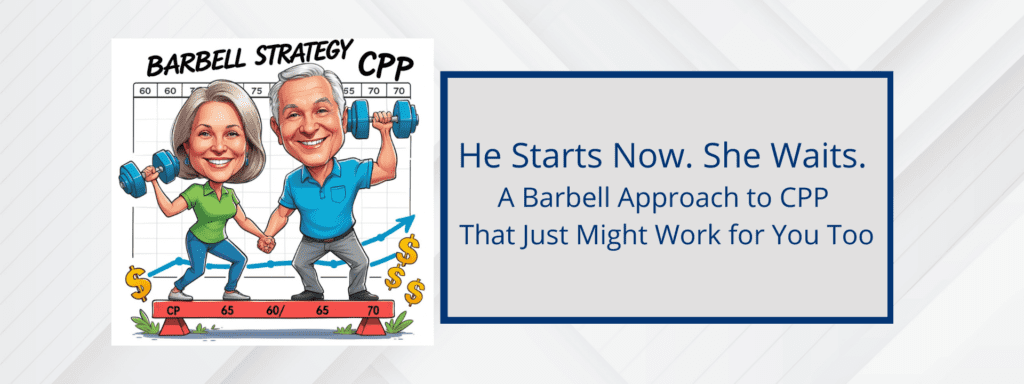

He Starts Now. She Waits. CPP and Retirement

A Barbell Approach to CPP That Just Might Work for You Too Ross and Rachel are a couple I’ve been working with for years. Rachel retired a while ago. Ross is planning to wrap up work at the beginning of 2026. He’ll have a fully indexed pension that covers their income needs pretty well—and they’ve […]

Why Every Retiree Needs a Bear Market Plan

Let’s be honest—market declines aren’t maybe in retirement. They are when. A typical retirement lasts 30 years, and during that time, there could be five or six bear markets. That’s five or six times the market could drop by 20% or more. And while we don’t know when those drops will happen, we do know […]

Three of our Best Insights for March

Our Monthly 3-2-1- Newsletter RESOURCE: Five Key Mindsets for the Transition to Retirement Our blog has grown tremendously over the last three years, with over 100 posts, each aimed at providing valuable insights into financial planning. In this compilation, I’ve selected the articles that stand out as essential reads on creating the mindsets for retirement […]

How to Avoid Losing Money in the Stock Market

Lately, market volatility has been making headlines, leaving many investors wondering what they should do. Should you sell? Hold steady? Make changes? Before making any big decisions, let’s break down what “losing money” really means and how you can protect your investments. What Does It Really Mean to “Lose Money”? When people say they’re “losing […]

If you are within 5 years of retirement, do this now!

Excerpts from the Book – Preserving Wealth – written by Jack Lumsden, MBA, CFP® Track your expenses!! If you are thinking about retiring within the next 5 years, you need to determine how much you spend in a year. Your day to day living expenses is the starting point to determine if you are on-track, […]

Three of our Best Insights for February 2025

Our Monthly 3-2-1- Newsletter RESOURCE: Nine Tax Strategies to Pay Less Tax in Retirement Your goal in retirement should be to organize your income stream to: The result will be greater spending for you today and potentially greater wealth for the next generation. RESOURCE: The Three Stages of Retirement Spending When retirement planning, you may want […]