“If I had Million Dollars” was a song released by the Bare Naked Ladies in 1992.

At that time, the majority of my friends had been married for few years, started to have kids, and perhaps started saving for retirement.

I heard the song the other day, and the last lyrics of the song are “If I had a million dollars, I’d be rich” and it got me thinking. So let’s say as a family you have saved a million dollars in your RRSPs, how much income would it provide today?

So I decided to do an “annuity check” to see what an immediate annuity would provide today as income. While I am not suggesting that everyone purchase an annuity with their RRSPs, the “annuity check” does provide a good benchmark on how much income you could generate today from a million dollar investment.

The following income chart is based on purchasing an annuity today for a million dollars for a couple. (Male and female)

What an annuity provides for the couple above, is that in exchange for the $1,000,000 from their RRSPs, they are guaranteed an income as long as one of them is alive. Each year the income is indexed (increases) by 2.0%. Upon the first death, the payments are reduced by 30%. This is basically purchasing your own pension.

Another way to check this is to review the projected maximum withdrawal rate today if you were to invest the $1,000,000, rather than buying an annuity. For example, if your total investments are $1,000,000, and you need to withdraw $25,000/year to cover all of you expenses and taxes, your initial withdrawal rate would be 2.5%. ($25,000/$1,000,000= 2.5 %).

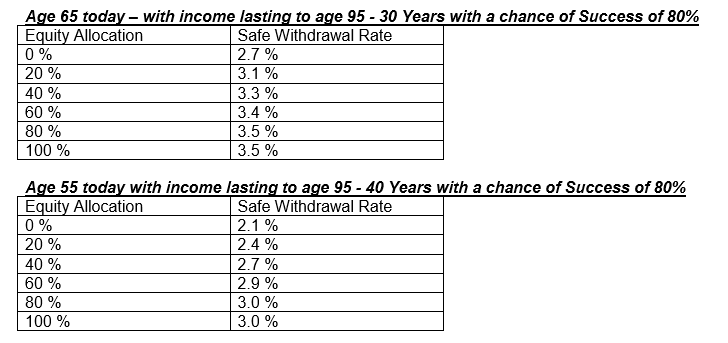

The following charts are from research by Morningstar Canada, and they are the projected safe withdrawal rates in Canada today. Below is a summary based on asset allocation and initial safe withdrawal rates that provides the retiree with an 80% chance of sustaining that rate over a 30 or 40 year period. (Potential time in retirement)

(Note: 80 % success rate means that 80 % of the time your money would last for the time period, and 20 % of the time, your capital would be depleted by the end of the time period).

Source: Safe Withdrawal Rates for Retirees in Canada Today, Morningstar January 2017. As an example, if you were both 55 years old today, and wished to plan to age 95 (40 years), and had a $1,000,000 investment account with an allocation of 60 % to equities, the safe withdrawal rate would be 2.9 % of $1,000,000, which is $29,000 per year. ($29,071 for the annuity at the same age today)

(For the full report see: Safe Withdrawal Rates for Retirees in Canada Today) So, the question to ask yourself is, if we are 55 years old today, with a million dollars, could you live on $29,000/year? Clearly, you would have to factor in Canada Pension Plan and Old Age Security, and any other pension incomes you may have. In other words “how much do you need to save on your own?”

So, while a million dollars is a lot of money, it may not provide as much income as you may think. In your financial plan, you have to determine how much capital you need to save in addition to your sources of guaranteed income (CPP/OAS/Pensions), to provide the lifestyle your family desires. If you don’t know how much enough is, contact your financial advisor to find this out, or contact us at jlumsden@assante.com for this essential analysis.